{kind=link}

Image this: You discover the proper house in East Nashville listed at $500,000. You are excited and able to make a proposal. However you then apply for a mortgage and notice the rate of interest in your mortgage issues far more than you assume.

At a 3% price (what patrons bought in 2021) and with a 20% down cost, your month-to-month cost—for principal and curiosity solely—can be round $1,686. At a 6.3% price immediately? That very same home prices you $2,476 per thirty days in curiosity and principal. That is round $790 extra each single month for the very same house.

Rates of interest change what you’ll be able to afford, how a lot competitors you face, and whether or not you can purchase or promote proper now. Once you’re researching the market, understanding these modifications might prevent tens of hundreds of {dollars}.

Here is what it’s essential find out about how rates of interest are shaping Nashville actual property in 2026.

For informational functions solely. All the time seek the advice of with a licensed mortgage or house mortgage skilled earlier than continuing with any actual property transaction.

Fast Takeaways: What Curiosity Charges Imply for You

Should you’re shopping for in Nashville:

- Present 6–6.5% charges scale back your shopping for energy by round 30% in comparison with 2021

- Ready for charges to drop might price you extra, as house costs preserve rising yearly

- Fee buydowns and vendor credit can offset greater charges

- Authorities-backed loans (which usually have decrease charges than standard) now supply greater limits: FHA as much as $943K, VA as much as $989K

Should you’re promoting in Nashville:

- Larger charges imply fewer patrons, however stock continues to be tight in lots of areas

- Aggressive pricing issues extra now than in 2021–2022’s vendor’s market

- Providing purchaser incentives like closing price assist or price buydowns attracts extra gives

- Your property fairness might help offset the upper price in your subsequent buy

Nashville Mortgage Charges in 2026: The place We Stand

Proper now, the nationwide common 30-year fixed-rate mortgage APR is round 6.3%. That is the place it’s settled after a wild few years, and mortgage price forecasts are predicting that they’ll keep within the low 6% vary for some time. Possibly dip ever-so-slightly beneath.

Again in 2020 and 2021, charges dropped beneath 3%. The pandemic pushed the Federal Reserve to maintain charges extremely low. Homebuyers might borrow cash cheaper than ever earlier than. That created a shopping for frenzy and a powerful vendor’s market—bidding wars, properties promoting in days, costs capturing up quick.

Then inflation hit onerous in 2022. The Federal Reserve raised charges to chill down the financial system. By late 2023, mortgage charges peaked above 7%. Consumers pulled again. The market slowed down.

Now, firstly of 2026, charges have stabilized. Consumers and sellers are beginning to settle for these charges as the brand new actuality. Individuals waited by 2023 and 2024, hoping for giant drops. That did not occur. And it in all probability will not.

The Federal Reserve has signaled it would make small price cuts, however mortgage charges do not mechanically comply with. Any decline can be sluggish and gradual.

Specialists predict charges will dip in 2026, however solely barely—maybe averages within the 5.5–6% vary. Returning to three–4% charges received’t occur anytime quickly.

What does this imply for Nashville? Consumers must price range primarily based on immediately’s charges, not hope for yesterday’s charges. Sellers want to know that patrons face greater month-to-month funds, which modifications negotiation dynamics.

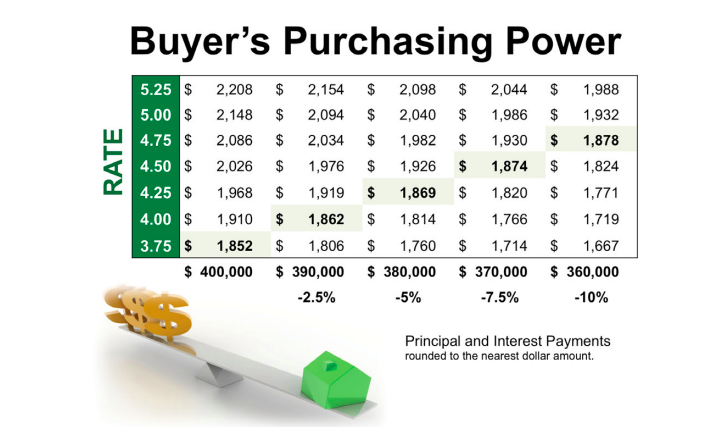

What a 6.3% Fee Actually Prices Nashville Consumers

Let’s take a look at actual numbers utilizing a $500,000 home and a 20% down cost (whole mortgage quantity: $400,000). For this comparability, we’re solely taking a look at principal and curiosity, not house insurance coverage or property taxes.

At 3% (what patrons bought in 2021):

- Month-to-month cost: $1,686.42

- Complete curiosity paid over 30 years: $207,109.81

At 6.3% (typical price in 2025):

- Month-to-month cost: $2,475.89

- Complete curiosity paid over 30 years: $491,320.82

That is $789.47 extra each month. Over the lifetime of the mortgage, you’ll pay an extra $284,211.01 in curiosity.

Here is one other method to consider it: you certified for a $400,000 mortgage at 3% in 2021 however determined the timing wasn’t proper. Now you wish to pull the set off, however you’re aiming for a similar mortgage cost that the 2021 numbers would’ve gotten you.

At a 6.3% rate of interest, you’d be restricted to a mortgage quantity of round $272,000. The homes you’re taking a look at? Round $340,000. In impact, you misplaced $160,000 in shopping for energy.

That is the 1/10 rule of rates of interest: for each 1% change in rate of interest, you’ll be able to anticipate to alter your homebuying price range by round 10%.

The revenue necessities modified dramatically as properly. Specialists suggest spending solely as much as 28% of your revenue on housing bills.

Together with estimated property taxes and house insurance coverage on a $500,000 property in Nashville, you’d want an annual revenue of round $127,600 to afford the house at 6.3%. In 2021, at 3%, you wanted about $93,700.

The Actual Price of Sitting on the Sidelines in Nashville

You is likely to be considering: “I will simply wait till charges drop to five% or decrease.”

Here is why that might backfire.

Nashville has a ton of pent-up housing demand. 1000’s of individuals delayed shopping for over the previous two years, ready for higher charges. They’re all sitting on the sidelines with you.

When charges DO drop—even to six%—all these patrons will bounce into the market directly. Extra patrons imply extra competitors. Extra competitors drives up costs quick.

The Math on Ready

For example you propose to attend a 12 months, hoping charges drop from 6.3% to five.5%. That will prevent about $205 per thirty days on a $400,000 mortgage.

However costs received’t keep regular throughout that point. Nashville house costs are projected to extend 2–4% in 2026. Should you’re taking a look at that $500,000 house immediately, it might price $510,000 to $520,000 subsequent 12 months.

Dwelling appreciation erodes your curiosity financial savings. At present, your month-to-month cost can be $2,475.89. Subsequent 12 months, best-case state of affairs, it might be $2,316.58—a financial savings of about $159, not $205.

And that’s if rates of interest drop that low. If, as some specialists forecast, the rate of interest stays regular all through 2026, you could be taking a look at a cost of round $2,575 subsequent 12 months, costing you an additional $100 per thirty days as a substitute.

Plus, when you wait, you are paying hire as a substitute of constructing fairness. Each month of hire is cash you may by no means get again. In the meantime, owners are constructing wealth by appreciation.

Bear in mind, you can begin constructing fairness now and refinance your mortgage if charges drop. If charges drop 1%, the financial savings usually offset the closing prices of the refi. (However at all times calculate to your personal scenario.)

Nashville’s Job Market Fuels Demand

Amazon and Oracle are increasing their Nashville workplaces in 2026. Healthcare continues to develop. The leisure business brings regular employment. Nashville’s unemployment price sits at round 3%, properly beneath the nationwide common.

Sturdy job development means folks preserve transferring right here. That retains housing demand excessive. Should you’re ready for some dramatic market crash or worth drop, Nashville’s financial fundamentals do not help that state of affairs.

The best way to Purchase Sensible When Nashville Charges Aren’t Budging

Larger charges do not imply you’ll be able to’t purchase. They imply you want smarter methods.

Negotiate Fee Buydowns from Sellers

That is big proper now. In early 2025, Redfin reported near-record highs of house gross sales with vendor concessions nationwide (round 44%). Vendor concessions remained a well-liked negotiating tactic by the housing market we’ve seen final 12 months. These concessions, when provided, are sometimes 1–3% of the house worth.

You need to use these credit to “purchase down” your rate of interest. Basically, you pay cash up entrance to completely decrease your price—1% of the mortgage quantity equals a 0.25% decrease price.

It’s essential to calculate the breakeven level of shopping for factors and consider how lengthy you propose to remain within the house. However should you’re shopping for for the long run, factors can prevent way over they price.

You can too take the out-of-pocket cash you save from vendor concessions and apply it to your down cost. Smaller mortgage, smaller month-to-month funds. It’s value it to run the mathematics to seek out your best choice.

Ask your agent to negotiate vendor credit into your supply. In immediately’s extra balanced market, sellers are sometimes keen to assist.

Contemplate Adjustable-Fee Mortgages

ARMs supply decrease charges for the primary 3, 5, or 7 years, then regulate primarily based on market circumstances. Should you plan to promote or refinance inside 5 years, a 5/1 ARM at 5.5% beats a 30-year mounted at 6.5%.

The chance is that if charges keep excessive and you do not promote, you would find yourself paying extra later. But when charges drop, you’ll be able to refinance right into a fixed-rate mortgage. Many Nashville patrons are utilizing ARMs as a bridge technique.

Store Totally different Nashville Neighborhoods

Your price range stretches in another way throughout Center Tennessee:

Rutherford County gives median costs round $424,000. That is roughly $50,000 lower than Nashville. Distant work makes the commute much less painful for a lot of patrons.

Sumner County averages round $439,000—a center floor between affordability and proximity to downtown Nashville.

East Nashville, The Nations, and Wedgewood-Houston supply appreciation potential should you can afford Davidson County costs. These neighborhoods are anticipated to outperform citywide averages.

Williamson County instructions premium costs close to $928,000 (not stunning with costly cities like Franklin and Brentwood), however stock stays tighter there.

Search for areas with 4–6 months of stock. Extra provide provides you negotiating leverage even when charges are greater.

Use Authorities-Backed Loans

Mortgage limits elevated for 2025:

FHA loans within the Nashville metro now go as much as $943,000 for single-family properties. You’ll be able to put down as little as 3.5% with a credit score rating of 580 (or 10% down with scores as little as 500).

VA loans for veterans and army households now permit as much as $989,000 with zero down cost in Davidson County.

USDA loans can be found in outlying suburbs and rural areas, providing 100% financing to eligible patrons with average incomes.

These applications make homeownership attainable for a lot of patrons even when charges are greater and houses price extra. As a result of these loans are assured by the federal government, they’re much less dangerous for lenders—and fewer danger interprets into decrease rates of interest.

Enhance Your Credit score Rating

Even small enhancements to your credit score rating matter. Lenders group their price tiers in brackets, not by each single level. Shifting from a 718 to a 720 credit score rating would possibly bump you up a tier and drop your price by 0.125% or extra. (Lender pricing matrices fluctuate, however that’s a standard common tier change.) That saves round $32 per thirty days on a $400,000 mortgage. Over 30 years, that is round $11,600.

Verify your credit score report for errors. Pay down bank card balances beneath 30% of your restrict. Arrange autopay. Do not open new credit score accounts whereas mortgage purchasing. Give your self 3–6 months to increase your credit score rating earlier than making use of.

Save a Bigger Down Cost

20% down eliminates non-public mortgage insurance coverage (PMI), which may price 0.3–1.5% of your mortgage yearly. That helps offset greater curiosity prices.

Plus, a bigger down cost usually will get you a barely higher price from lenders.

Promoting Your Nashville Dwelling? Charges Change Your Technique

Should you’re promoting, greater charges have an effect on you in another way than patrons—however they nonetheless matter.

The Fee Lock-In Impact

As of late 2025, about 54% of U.S. owners nonetheless have locked-in mortgage charges beneath 4%. Possibly you are one in every of them. The concept of promoting your 3.5% mortgage and getting a brand new one at 6% feels painful.

These “golden handcuffs” have put a squeeze on stock for years. As a substitute of buying and selling up or downsizing and itemizing their outdated properties on the market, owners have been staying put. Whereas the share of householders with these traditionally low charges has been slowly reducing as life occasions drive gross sales, it’s nonetheless locking up a major variety of homes.

However here is what sellers neglect: your house fairness.

For example you obtain in 2020 for $350,000 at 3%. Your property is now value $490,000. You’ve $140,000 in fairness (plus no matter you paid down on the principal).

Have your sights on a $500,000 house? A 20% down cost prices simply $100,000 of that fairness—with nothing out of your financial savings account. And you continue to have revenue left over to speculate, purchase factors, or apply towards principal.

You are not shedding your low price—you are utilizing the wealth it helped you construct. Your fairness lets you relocate for a better-paying job, transfer someplace you’ve at all times wished to stay, or purchase a home that higher fits your wants.

2026 Nashville Promoting Actuality

The Nashville actual property market has modified. It is not the loopy vendor’s market of 2021–2022.

Stock is up round 16% year-over-year in Nashville correct. Extra properties are sitting in the marketplace longer. The common days on market is over a month.

Properties are promoting nearer to record worth—or beneath it. Value reductions have gotten extra frequent. Nationally, over 25% of listings have been getting worth cuts in current months. Nashville is not immune.

What does this imply? Pricing technique issues extra now. You’ll be able to’t overprice and anticipate bidding wars to bail you out. Consumers are extra cautious. They’re evaluating choices rigorously. They’re negotiating tougher.

However do not panic. Nashville nonetheless has robust fundamentals. Properties are promoting. You simply want the proper strategy.

Value It Proper, Sweeten the Deal, Promote Quicker

Aggressive Pricing from Day One

Overpricing kills momentum quick. Consumers see your overpriced itemizing. They cross it by. It sits. After a number of weeks, patrons surprise what’s flawed with it. You find yourself chopping the worth anyway, however now you’ve got misplaced the perfect patrons and wasted helpful time.

Again when patrons had been scrambling to lock in low charges, you may need been in a position to get away with an over-market worth. Now, when purchaser budgets are already squeezed with greater funds? Not an opportunity. At present’s patrons are extraordinarily budget-conscious.

Work with an agent who is aware of your particular Nashville neighborhood. Do not worth primarily based on what your neighbor bought in 2022. That was a distinct market. Base your asking worth on comparable properties in your space that bought within the final 60–90 days at present charges.

Value competitively from day one. You will entice extra showings, extra gives, and promote sooner.

Provide Purchaser Incentives

Closing price help is changing into extra frequent in Nashville. You can too supply price buydowns. That is the place you pay cash at closing to cut back the customer’s rate of interest. A 1% buydown will price you a number of thousand, however it may very well be the distinction between getting a proposal or not.

That is particularly essential whenever you’re promoting to a first-time homebuyer. With out fairness from a earlier house sale, first-time patrons are particularly receptive to something that reduces their preliminary shopping for prices.

Dwelling warranties give patrons peace of thoughts about home equipment and methods. Restore allowances let patrons sort things their method somewhat than negotiating each small subject throughout inspection.

These incentives price you cash, however they promote properties sooner. A sooner sale usually nets you extra money than sitting in the marketplace for months.

Make It Transfer-In Prepared

First impressions matter extra when patrons are nervous about month-to-month funds. They do not wish to see a fixer-upper that wants $20,000 in quick out-of-pocket repairs.

Sensible house options entice millennial patrons, who make up an enormous portion of the market. A sensible thermostat, doorbell digicam, and safety system aren’t costly within the grand scheme of issues however sign a contemporary, up to date house.

Vitality-efficient upgrades attraction to Nashville patrons frightened about rising utility prices. New home windows, up to date HVAC, and higher insulation decrease month-to-month working prices, which helps offset greater mortgage funds.

Skilled staging helps patrons visualize residing in your house. It feels counterintuitive, however empty rooms look smaller. Cluttered rooms look messy. Staged rooms look aspirational. Staged itemizing pictures get extra consideration and provide help to promote sooner.

Be Versatile on Phrases

Regulate closing timelines to match purchaser wants. Some want 60 days to promote their present house. Others wish to shut in 30 days. Being versatile attracts extra gives.

Be open to negotiation on inspection objects. In immediately’s market, patrons anticipate sellers to deal with affordable restore requests. Do not dig in your heels over $500 value of fixes when it might price you the sale.

For informational functions solely. All the time seek the advice of with a licensed mortgage or house mortgage skilled earlier than continuing with any actual property transaction.

Your Subsequent Steps in Nashville’s Market

Rates of interest change the sport. 6% charges are a actuality for 2026, and the excessive borrowing prices in comparison with current years are affecting each patrons and sellers.

However Nashville’s actual property market continues to be lively, properties are nonetheless promoting, and patrons are nonetheless discovering properties they love. You simply want the proper technique and sensible expectations.

If the alternatives of Nashville excite you, contact The Ashton Actual Property Group of RE/MAX Benefit with Nashville’s MLS at (615) 603-3602 to get in contact with native actual property brokers who might help discover the proper Nashville house for you immediately.